|

If you’re buying or selling a home, one of the biggest steps in the process is the home appraisal. It’s the moment when an expert steps in to answer a simple but crucial question: what is this home really worth?

At Cross Street, we know the appraisal can feel like a mystery, especially if it’s your first time. That’s why we’re breaking down what a home appraisal is, how the home appraisal process works, who typically pays for a home appraisal, and what buyers and sellers should expect.

A home appraisal is an independent estimate of a property’s value, ordered by the lender as part of the mortgage process. While your real estate broker helps you understand what a home is likely to sell for through a comparative market analysis, the appraisal serves a different purpose.

A home appraisal is the bank’s way of confirming that the agreed-upon price reflects the home’s actual value, and that they’re not lending more than the property is worth. In simple terms, the market value suggested by comparable market analysis shows what buyers are willing to pay, and the appraisal helps verify that number before the loan is approved.

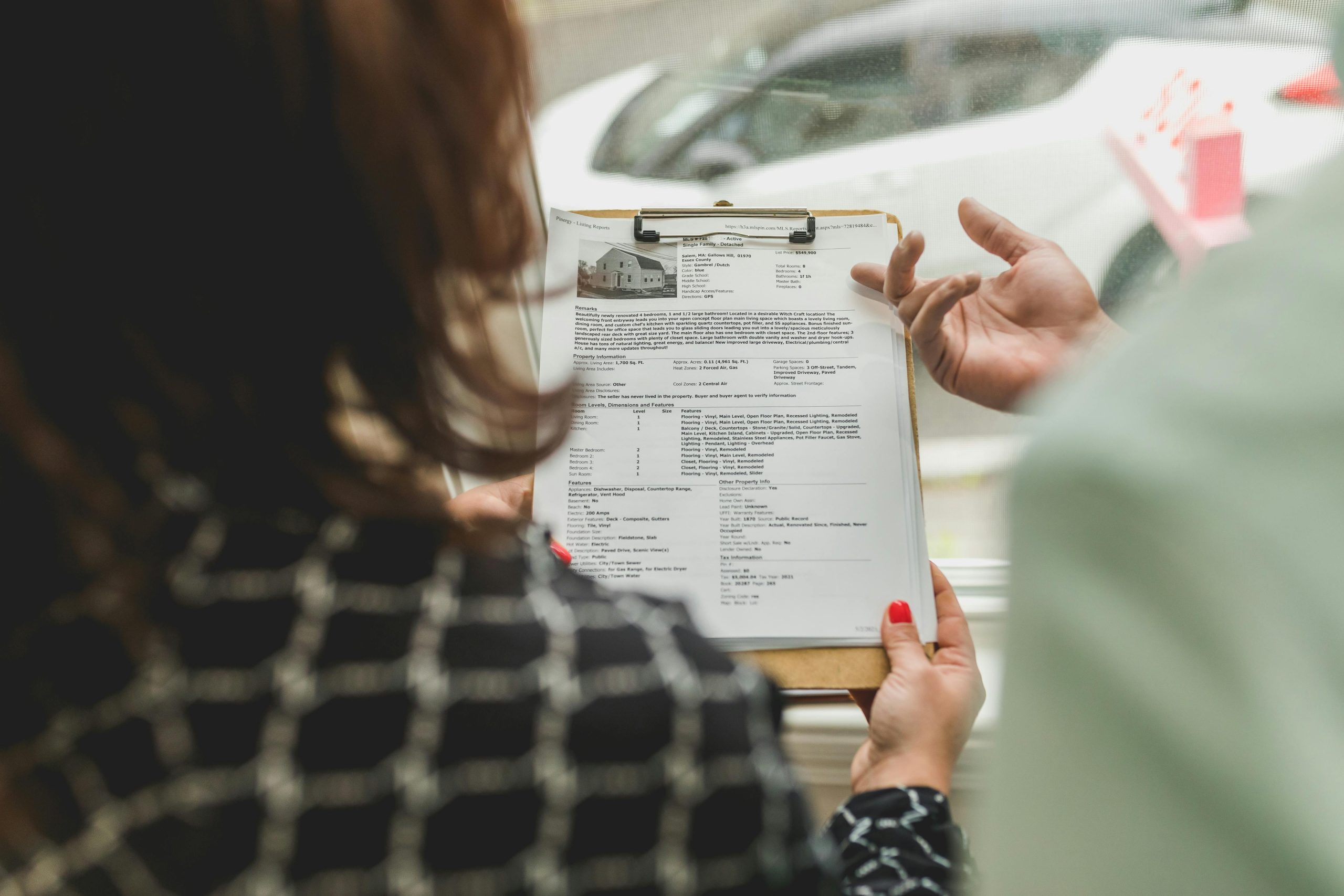

Once the appraiser has inspected the property and analyzed the comps, they compile their findings into a home appraisal report. This document can seem overwhelming, but knowing what to look for makes it much easier to understand and use effectively.

Here are the most pertinent sections and what they mean:

Final Appraised Value

Comparable Sales or “Comps”

Adjustments

Condition Notes

Neighborhoods and Market Data

Understanding the report is one thing, but what happens once you receive it? Let’s explore how the appraisal affects the sale itself.

A common concern for buyers and sellers is what happens if the appraisal doesn’t match expectations. Here’s how to navigate different scenarios:

Appraisal meets or exceeds the purchase price

Appraisal comes in below the purchase price

This can feel stressful, but there are multiple options:

Why the buyer might bring extra cash

Most of the time, the buyer pays for the home appraisal as part of their closing costs. A new home appraisal is also required for refinances, and the homeowner is responsible.

In most home purchases, the buyer pays for the home appraisal as part of their closing costs. Think of it as an investment in peace of mind: the appraisal ensures the property is worth the price you’ve agreed to pay, which protects both you and the lender.

For refinances, the responsibility falls on the current homeowner. Lenders require an updated appraisal to determine your home’s current value and how much equity you have, which helps set the terms of your new loan.

Most appraisals range between $300 and $600, though costs can vary widely depending on the property type and location. Here are some of the key factors that can impact the price:

Beyond individual transactions, appraisals serve a larger role in stabilizing the real estate market.

Market balance: Appraisals help prevent overpricing in hot markets and underpricing in slower areas. They provide an unbiased measure of a home’s value.

Informed decisions: By understanding appraisal trends, buyers, sellers, and lenders can make better financial decisions.

Equity tracking for refinancers: Homeowners looking to refinance can see a realistic estimate of their equity, which is crucial for smart financial planning.

An appraisal tells you what the home is worth. An inspection tells you what condition it’s in. Both matter, but they serve different purposes.

The property visit itself takes less than an hour. The full process, including research, analysis, and report, can take up to two weeks.

Yes. You (or your lender) can request a reconsideration of value, usually by providing additional comparable sales.

In purchases, the buyer covers the cost. In refinances, the homeowner does.

There are a few options: the seller can lower the price, the buyer can cover the difference in cash, or either party may decide to walk away.

Buying or selling a home comes with a lot of moving pieces. At Cross Street, we’re here to walk you through every step, from the appraisal to the closing table, so you feel confident in your next move.

Join our mailing list to receive notifications every time a new blog post is live.